Geopolitical instability halfway around the world may seem distant from your local gun counter or online cart, but the connections are real, measurable, and worth understanding.

This one’s a little different. If you’re a regular here, you already know we don’t shy away from the deeper side of the industry, and this article is for exactly that kind of reader. Instead of the usual product focus, we’re getting into the data: government disclosures, commodity markets, and what the numbers are actually telling us about where the 2A industry is headed. My goal is to give you a clear, non-partisan, honest picture of what’s going on and why it matters. Hope you find it as interesting as I did putting it together.

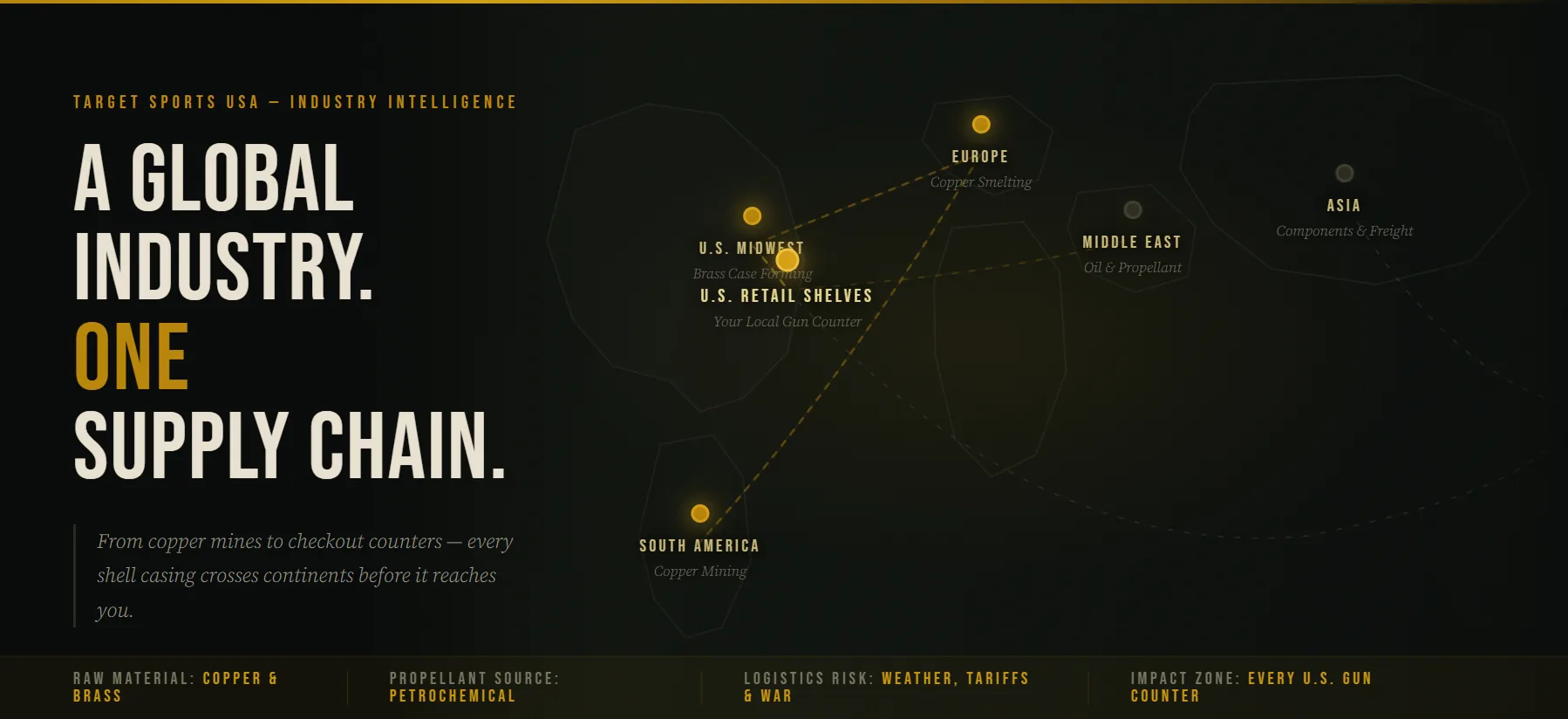

Why Global Events Always Hit American Shelves

The U.S. firearms and ammunition industry doesn’t operate in a vacuum. Copper mined in South America gets smelted in Europe, shaped into brass cases in the Midwest, and loaded into cartridges that end up on shelves in every state in the country. Gunpowder relies on petrochemical derivatives. Freight ships carry component materials across oceans on schedules subject to weather, tariffs, and war.

Since the Hamas attack on Israel on October 7, 2023, and the subsequent escalation involving Iran and increased U.S. military engagement in the region, a set of interrelated pressures has been building throughout the global supply chain. None of them, individually, constitutes a crisis for American shooters. But taken together, they represent a meaningful shift in the cost and logistics landscape that every serious gun owner, hunter, and competitor should understand.

It is also worth noting that the U.S. government retains the authority to invoke the Defense Production Act of 1950 (P.L. 81-774, 50 U.S.C. §§4501 et seq.), which could be used to prioritize military ammunition output over civilian supply, a scenario that would put direct pressure on domestic stockpiles.

This article breaks down each of those pressures, from military procurement to raw material prices to Red Sea shipping disruptions, using publicly available data and industry reporting.

Key Takeaways

- Ammunition prices are elevated and unlikely to reverse soon. Copper is up 50-60% since early 2023, and propellant supply remains constrained globally.

- Civilian supply is currently stable. Unlike 2020-2021, shelves are stocked, and inventory levels are healthy.

- The U.S. military has largely expanded production capacity rather than redirected civilian output, but the Defense Production Act remains an available lever that could change that quickly.

- Red Sea shipping disruptions are not affecting finished ammunition bound for U.S. retail, but are quietly inflating upstream costs for raw materials and components.

- Historical precedent is reassuring, past Middle East conflicts did not produce civilian ammo crises, but that holds only as long as pressure points don’t stack simultaneously.

- An escalation involving Iranian oil infrastructure or further Red Sea deterioration remains the most direct trigger for accelerated price pressure on U.S. ammunition.

U.S. Military Aid to Israel and the Domestic Supply Chain

Since October 7, 2023, the United States has provided at least $21.7 billion in military aid to Israel, according to Brown University’s Costs of War Project. This figure encompasses bombs, missiles, artillery shells, and small arms ammunition across multiple aid packages authorized by Congress and executed through Pentagon drawdown authorities.

| Category | Amount |

|---|---|

| U.S. Military Aid to Israel | $21.7 Billion |

| U.S. Military Operations in Yemen, Iran, and the Wider Middle East Region | $9.65 – $12.07 Billion |

| Total | $31.35 – $33.77 Billion |

A breakdown published by the Security Assistance Monitor in August 2025 identified approximately $416 million of that aid as falling under the “firearms” category, covering small-arms systems and related ammunition, with the balance concentrated in air-delivered munitions and artillery.

The immediate question for American gun owners is straightforward: Does arming an ally overseas reduce what’s available here at home?

The answer, based on available evidence, is nuanced. The U.S. government has not publicly released line-item tallies of specific calibers shipped to Israel: figures for 5.56 NATO, 9mm, or .308 rounds sent abroad have not been broken out in any official disclosure. Aid is grouped under broader “drawdown” and Foreign Military Financing (FMF) designations, making a direct inventory-level comparison to civilian market supply essentially impossible with public data.

What is clear is how the government has managed domestic production to meet both needs simultaneously. Major manufacturers like Olin Winchester hold long-term U.S. Army contracts for small-caliber ammunition at the Lake City Army Ammunition Plant in Missouri, covering 5.56mm, 7.62mm, .50 BMG, and the newer 6.8mm cartridge. Rather than pulling capacity away from civilian markets, the Pentagon has funded facility expansions, including a 450,000-square-foot production complex at Lake City specifically for 6.8mm output, to grow the overall pie rather than redistribute a fixed one.

On the commercial side, The Kinetic Group, formerly Vista Outdoor’s sporting products division and home to Federal, Remington Ammunition, CCI, and Speer, was acquired by the Czechoslovak Group in a deal valued between $1.91 and $2.15 billion. Despite the foreign ownership, U.S. manufacturing operations remain intact and active. Federal, for instance, holds a contract with U.S. Customs and Border Protection for up to 143 million rounds of 5.56mm duty ammunition over five years, a significant government commitment running parallel to robust civilian production.

The bottom line on military procurement: the evidence does not support a narrative of direct military-to-civilian supply cannibalization. The impact is more subtle: it shows up in manufacturing capacity allocation, energy costs, and raw material demand, not empty shelves from diverted pallets.

Raw Material Prices: Copper, Brass, Lead, and Energy

The real, measurable impact of the Middle East conflict on your ammunition costs runs through commodity markets, and the numbers are significant.

Copper and Brass

The cartridge case is the single most material-intensive component of a round of ammunition. Brass cases are typically composed of 70% copper and 30% zinc, which means copper prices function almost as a direct input cost multiplier for ammunition manufacturers.

Since early 2023, LME copper prices have risen from roughly $8,000–$8,500 per metric ton to approximately $12,500–$13,500 per metric ton by early 2026, an increase of roughly 50 to 60 percent. As of late February 2026, cash copper prices were trading above $13,200 per metric ton, indicating continued upward pressure with no clear near-term reversal.

Middle East instability contributes to this through two channels: oil-price-driven energy costs (copper smelting is energy-intensive), and broader financial market volatility that drives capital toward commodities as a hedge. Higher copper prices mean higher brass prices, which means higher per-round manufacturing costs, a reality that filters through to retail over time.

Lead

Lead, used for bullet cores in the majority of commercial ammunition, has shown more modest movement. LME lead prices have held in the $2,000–$2,100 per metric ton range through early 2026, oscillating without dramatic spikes. The moderate increase still adds incremental cost per round for high-volume calibers like 9mm and .223 Remington, where margins are thinnest, and volume is highest.

Oil, Energy, and Gunpowder

This is perhaps the most direct geopolitical link to your ammunition costs. Middle East instability has kept Brent crude trading in the $80–$100 per barrel range since late 2023, with occasional spikes above $100 during escalatory events.

Oil prices affect ammunition manufacturing across multiple vectors: electricity costs at production facilities, transportation of raw materials and finished goods, and, critically, propellant production.

Smokeless powder is derived from nitrocellulose, a petrochemical-adjacent product whose manufacturing cost is sensitive to energy input prices. Industry analysts and manufacturer commentary have flagged a “global gunpowder shortage” driven by the convergence of elevated energy costs and the surge in worldwide military demand, with conflicts in the Middle East and Eastern Europe creating simultaneous procurement pressure on propellant suppliers.

Vista Outdoor (The Kinetic Group) specifically cited this dynamic when announcing that ammunition prices would “rise substantially” back on January 1, 2024, and again on October 1, 2025 and guess what, again this year, April 1, 2026 attributing the increase in part to powder supply constraints and energy-driven cost inflation.

Want our full outlook on 2026? Back in December, I was able to put together a detailed breakdown covering everything from supply conditions to market signals, check out Ammunition in 2026: Supply Conditions, Price Pressures, and Market Signals.

Red Sea Disruptions: Shipping Lanes Under Fire

From November 2023 to the present day, March 2026, Houthi forces in Yemen, operating with Iranian support, began targeting commercial shipping in the Red Sea, Gulf of Aden, and Persian Gulf. This corridor represents one of the most critical maritime trade lanes in the world, connecting Asian manufacturing and European markets through the Suez Canal.

The war in Iran is choking off a key shipping route in the global supply chain, potentially leading to massive delays in the flow of goods to American consumers, this include one-fifth of the world’s oil supply. There has also been reports of Iran stating they will set fire to any ship that is passing through.

Source: NBC News “Iran-U.S. war chokes key shipping lane and threatens global cargo industry“

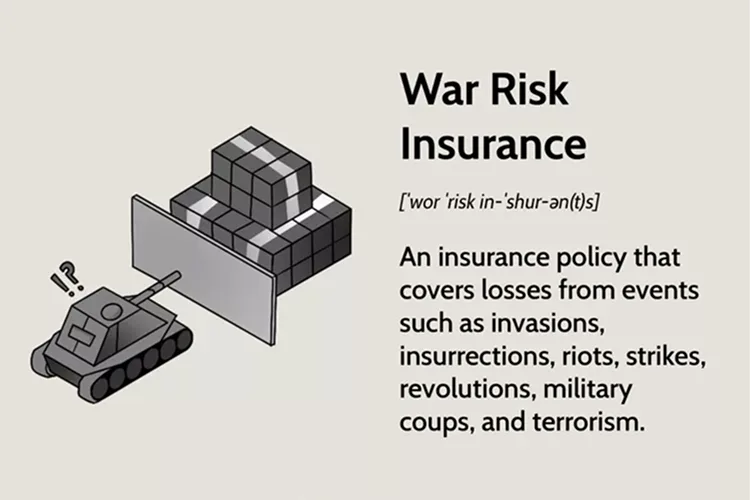

The operational impact has been significant. Rather than risk attack, most major carriers have rerouted vessels around the Cape of Good Hope, adding 10 to 14 days to voyage times and corresponding increases in fuel, crew, and operating costs. Container shipping rates along Asia-Europe lanes more than doubled at peak disruption, and while spot rates have since moderated, they have not returned to pre-crisis levels.

War-risk insurance premiums for vessels still transiting the Red Sea jumped from approximately 0.3% of a ship’s insured value to 0.7–1.0%, adding hundreds of thousands of dollars in incremental costs per voyage. Some insurers have partially suspended coverage entirely for Red Sea routing.

For the ammunition industry specifically, the linkage is indirect but real. There is no evidence that finished commercial ammunition destined for U.S. retail is routinely shipped via the Red Sea, as most imports arrive through Pacific or Atlantic gateways. However, raw materials and components, including copper, zinc, and specialty chemical additives, that originate in Asia or pass through the region are subject to higher freight and insurance costs. Those costs are absorbed by suppliers and passed along the chain, contributing to the broader “geopolitical risk premium” now embedded in many manufacturers’ cost models.

Consumer and Retail Trends: Demand in a Post-Boom Market

For context on how the civilian market is responding, it helps to look at the hard numbers, and they tell a story of normalization rather than panic.

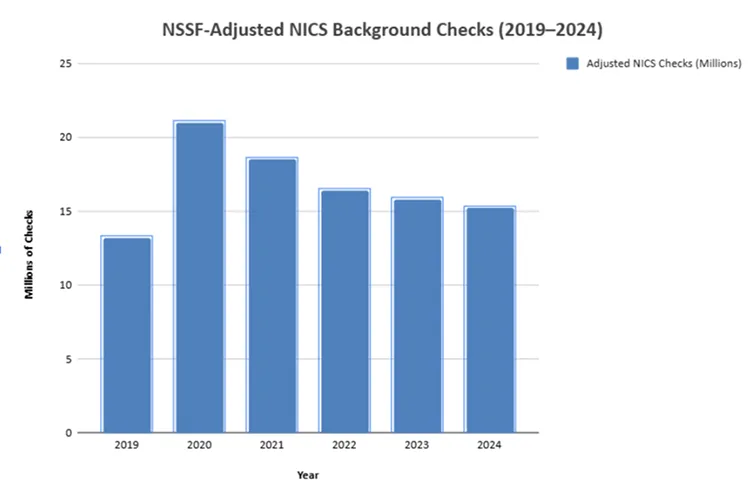

NICS-adjusted background checks, the most reliable public proxy for firearm sales, fell from 15.8 million in 2023 to 15.2 million in 2024, a 3.5% year-over-year decline. This is consistent with the broader post-pandemic normalization underway since the record-setting years of 2020 and 2021. The current conflict in the Middle East has not, in itself, triggered a civilian buying surge comparable to past domestic shock events.

| Year | Adjusted NICS Checks (Millions) | YoY Change |

|---|---|---|

| 2019 | 13.2 | — |

| 2020 | 21 | 59.1% |

| 2021 | 18.5 | -11.9% |

| 2022 | 16.4 | -11.4% |

| 2023 | 15.8 | -3.7% |

| 2024 | 15.2 | -3.8% |

That said, the NSSF’s 2024 Economic Impact Report shows total industry economic activity growing from $90.1 billion in 2023 to $91.7 billion in 2024, reflecting continued revenue growth from ammunition, accessories, and services even as new firearm unit sales decline, a sign of a maturing market with a deeply engaged consumer base.

On the ammunition retail side, RetailBI data tracked through late 2023 showed a complicated picture: inventory was up approximately 6% year-over-year, while sales were down about 9%, and average prices paid had declined roughly 11%. Paradoxically, 28% of consumers surveyed reported ammunition as “less available” despite inventory being higher, a perception gap likely rooted in the lingering memory of the 2020–2021 shortage era, when shelves were genuinely bare.

| Metric | Change (YOY) |

|---|---|

| Inventory | +6% |

| Sales Volume | -9% |

| Average Price Paid | -11% |

Major retailers like ourselves at Target Sports USA, Bass Pro Shops, and Cabela’s have not issued formal statements attributing specific price movements to Middle East events. Retail pricing tends to be insulated in the short term by multi-million-round, fixed-term contracts with manufacturers, but those prices renegotiate, and the input-cost pressures described above will eventually find their way to the shelf.

What the Industry Is Saying

Official industry bodies have been measured in their public commentary. NSSF and SAAMI have not issued statements explicitly linking the Israel-Iran-U.S. conflict to an ammunition shortage or price crisis. NSSF’s public messaging has focused on domestic demand normalization, framing current market conditions as the inevitable cooling of the pandemic-era boom rather than a response to geopolitical shocks.

Publicly traded manufacturers have been somewhat more candid in their investor-facing communications. Both The Kinetic Group and Olin Corporation have flagged geopolitical tensions in their 10-K filings and investor materials as a structural demand driver, but frame it as a positive for long-term revenues, not a near-term supply problem. The expansion of military and law enforcement contracts is presented as additive capacity growth, not a diversion from civilian production.

Independent equity research, notably Gabelli’s “State of the Great Outdoors 2024” analysis, describes the period since 2023 as an “ammo war” among strategics, with large ammunition assets being acquired partly to position for NATO and U.S. restocking programs driven by multiple simultaneous conflicts. This framing makes clear that while geopolitical tensions are structurally bullish for the industry, they also carry input-cost and logistics risks that will compress margins in the near term.

The global ammunition market is projected to grow by approximately $3.9 billion between 2024 and 2028, according to Technavio market analysis, with geopolitical conflicts and ongoing tensions cited as primary demand drivers.

Historical Perspective: This Isn’t the First Rodeo

American shooters have lived through multiple periods of elevated military demand, and it’s instructive to see how past conflicts shaped the civilian market.

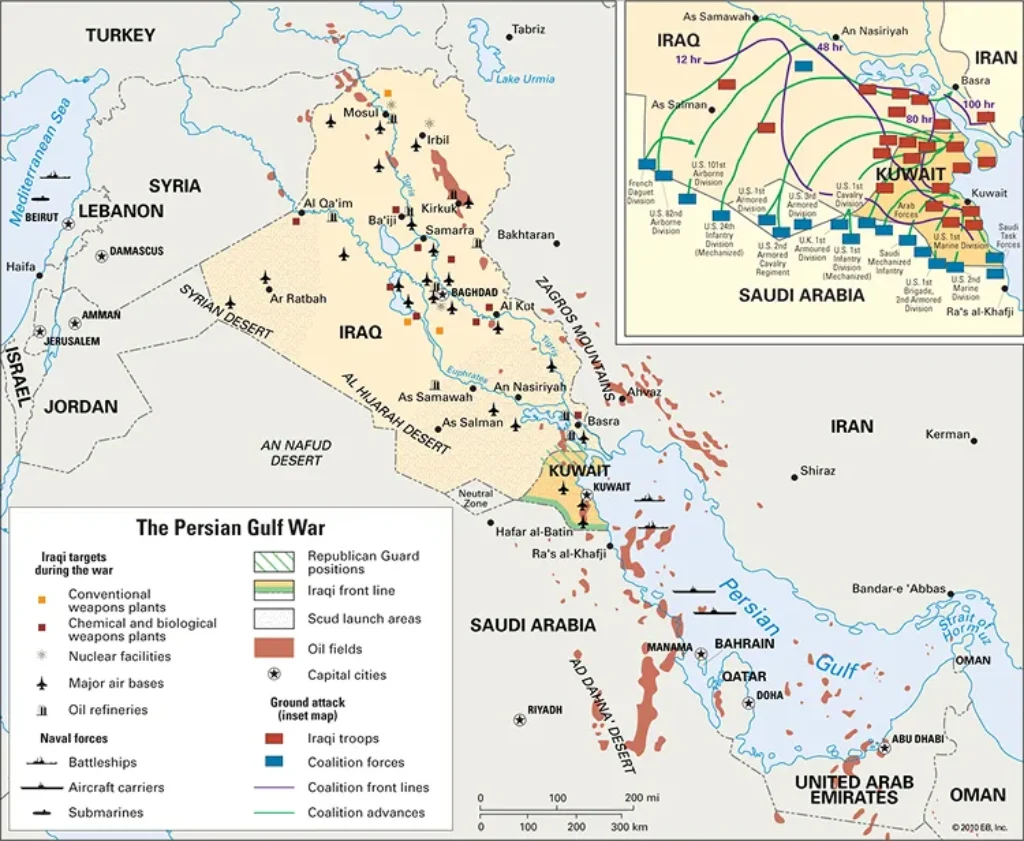

During the Gulf War (1990–1991) and the subsequent Iraq War (2003–2011), U.S. military ammunition demand spiked considerably. Yet neither conflict produced a sustained civilian shortage or significant price disruption. The government drew from existing stockpiles and ramped production on parallel tracks, and the commercial market continued to operate without major interruption.

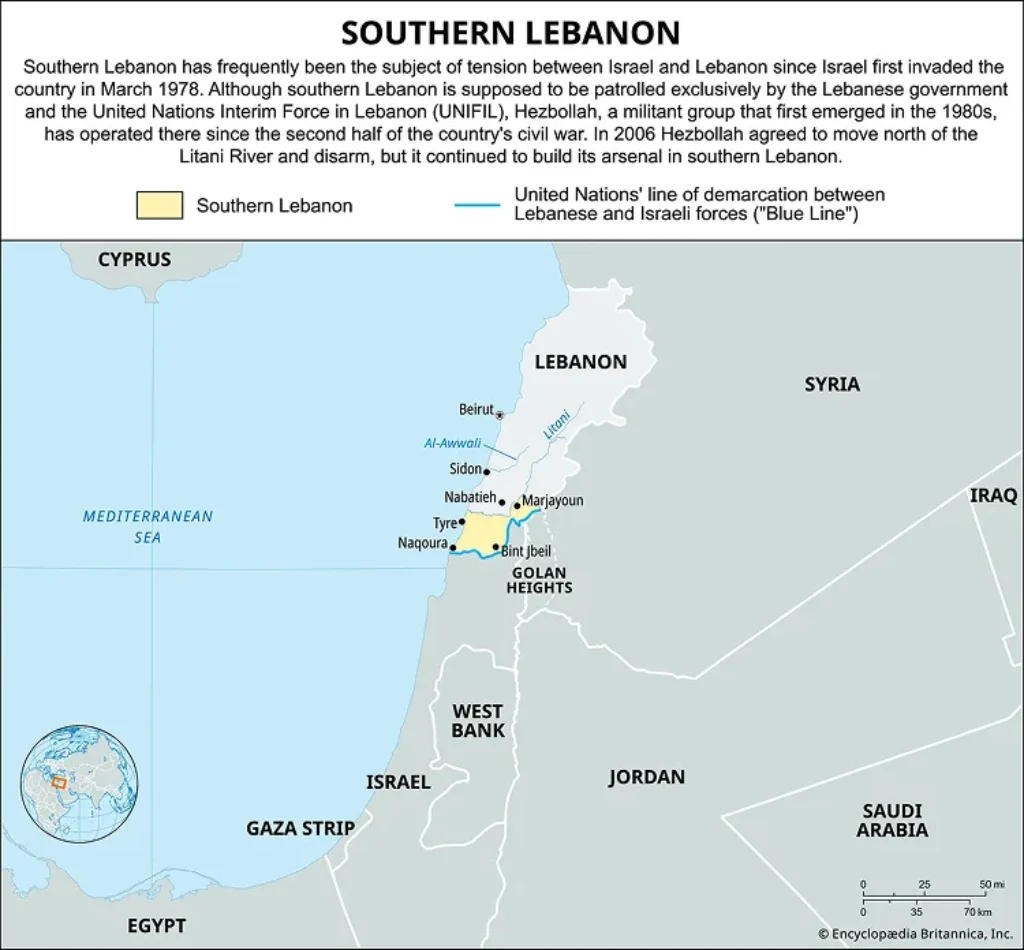

The 2006 Lebanon War and other regional flare-ups generated modest upticks in procurement but left no visible signature in civilian ammunition pricing data.

The most disruptive episode in recent U.S. ammunition history, the 2020–2021 shortage, was not primarily driven by military demand at all. It was a product of pandemic-driven panic buying, political uncertainty, a surge of first-time gun buyers, and supply-chain breakdowns across manufacturing and logistics simultaneously. Military procurement was a contributing factor, but not the primary cause.

The lesson from history is that geopolitical conflicts tend to extend demand cycles and raise input-cost floors, but they don’t, by themselves, create hard supply crises, unless they’re layered on top of other domestic shocks. The 2024–2026 environment looks more like the former than the latter.

What This Means for American Shooters

Here’s the practical takeaway from everything we just saw above:

Expect moderate, sustained price pressure, not a crisis. The convergence of elevated copper prices, higher energy costs, gunpowder supply constraints, and increased logistics costs represents a genuine structural shift in manufacturing economics. That won’t reverse quickly. Ammunition prices are unlikely to return to 2019 levels anytime soon, and the input pressures described here are not going away as long as Middle East instability persists.

Supply is not critically constrained. Unlike 2020–2021, shelves are stocked. Inventory levels at the retail level have been elevated, not depleted. The availability perception gap noted in consumer surveys is a psychological holdover from the shortage era, not a reflection of current reality.

Watch energy markets. The most direct, real-time indicator of where ammunition input costs are headed is the oil price. A sustained spike above $100 per barrel on Brent, especially if triggered by an escalation involving Iranian oil infrastructure, would represent the most immediate upward pressure on manufacturing costs.

Buy what you need, not what you fear. The dynamics described here are real and worth understanding, but they don’t justify panic purchasing. The industry has demonstrated, through the Gulf War, Iraq War, and even the early COVID period, that it can expand production to meet demand when conditions require it. Domestic manufacturing capacity has been growing, not shrinking.

Stay informed. The situation in the Middle East remains fluid. U.S. military involvement, Iranian nuclear posture, and Houthi activity in the Red Sea are all variables that could shift the calculus described here. Following credible industry reporting, not social media speculation, is the best way to stay ahead of genuine supply or pricing changes.

What Does All of This Mean in the End?

The Israel-Iran-U.S. conflict and broader Middle East instability are not abstract news events for the American firearms community. They are part of a web of economic forces, including commodity prices, energy markets, military procurement, and global shipping, that connects geopolitical events to the price you pay per box of ammunition.

The good news is that the U.S. ammunition industry has proven resilient across multiple cycles of elevated military demand, and current evidence points to moderate price pressure and margin compression rather than crisis-level supply disruption. Manufacturers are expanding, not contracting. Shelves are stocked. And the structural demand drivers that benefit the industry long-term are the same ones creating near-term cost headwinds, a tension the market has navigated before.

Understanding these dynamics makes you a better-informed consumer, a more rational buyer, and a more credible voice in conversations about the industry you’re part of.

Kailon Kirby covers the ammunition market for Target Sports USA, where he has a view most writers never get. Working inside one of the country's largest online ammo retailers, he tracks pricing movements, supply conditions, and brand-level shifts as they happen, not after the fact.

A Connecticut State Pistol Permit and Concealed Carry holder, Kailon isn't just watching the numbers. He shoots, he carries, and he understands what market changes actually mean for the person standing at the counter or checking out online. That combination of ground-level industry access and shooter perspective is what shapes everything he writes.

When something is moving in the ammunition market, Kailon is usually the first to see it.

- Kailon Kirby

- Kailon Kirby

- Kailon Kirby

- Kailon Kirby